When AI means business

AI is rewriting the rules of finance, with 92% of firms seeing it pay off. But while some functions soar, others stall. What’s driving success and where the biggest challenges remain?

-

Marina Mouka

- December 3, 2024

- 5 minutes

The adoption of artificial intelligence (AI) across finance functions globally has reached unprecedented levels, according to KPMG’s latest survey, which paints a detailed picture of the current state of AI implementation and its potential to reshape financial processes. The findings, drawn from a survey of 2,900 companies across 23 countries and 6 industries, highlight both the achievements and the challenges faced by organisations in integrating AI into their operations.

The report, AI in Finance: Transforming into a New Era with the AI-Empowered Finance Function, reveals a significant milestone:

- 71% of companies surveyed are using AI within finance operations.

- 58% are piloting or deploying generative AI (GenAI).

- 92% report that their finance function’s AI initiatives are meeting or exceeding return on investment (ROI) expectations.

“AI is becoming more important than ever to enhancing quality, mitigating risks and enabling deeper, data-driven insights,” said Thomas Mackenzie, KPMG US and Global Audit Chief Technology Officer.

Why tax is stuck in the slow lane

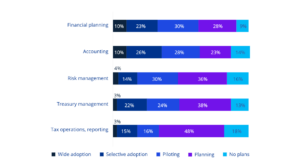

While AI is making strides across a range of finance functions, the survey shows that progress is not uniform. Companies have made the most headway in leveraging AI for financial planning, with 78% piloting or using AI in this area, followed closely by accounting (76%). Treasury management has also seen substantial adoption, with 64% of organisations using AI to improve cash flow forecasting, fraud detection, and credit risk assessment.

Progress made in the use of AI in finance areas. Source: KPMG

In contrast, AI adoption for tax and operations remains limited, with only 45% of companies reporting active use. KPMG attributes this disparity to the inherent complexities of tax regulations, reliance on legacy systems, and the need for human judgement in many tax-related decisions.

Brad Brown, KPMG US Chief Technology Officer – Tax, acknowledged these challenges, noting that “tax leaders are eager to unlock the transformative potential of GenAI for their tax departments, but the complexity of the current landscape can make this path seem daunting.”

AI leaders turn data into gold

KPMG’s report introduces a maturity framework to classify organisations into three categories: AI leaders, middle ground implementers, and beginners. Among the companies surveyed, 41% are identified as AI leaders, a group that consistently achieves higher-than-expected ROI. In contrast, only 33% of beginners and middle-ground implementers report similar outcomes.

AI leaders distinguish themselves through both investment and resourcing strategies. They dedicate approximately 13% of their IT budgets to AI-related activities—significantly more than their counterparts—and are projected to increase this share to over 17% in the next three years. Additionally, they combine internal resources, such as centralised AI teams, with external expertise to accelerate their AI journey.

These leaders report a broader range of benefits, from faster insights and improved decision-making to enhanced productivity and operational efficiency. “The benefits of AI compound as firms continue to invest in new capabilities and embed AI into their financial reporting processes,” Mackenzie explained.

Cloud makes way for AI

Despite AI’s rising prominence, cloud technology remains the top priority for enhancing financial reporting processes. However, its dominance is beginning to wane. While 77% of finance leaders prioritised cloud migration in May, this figure has since dropped to 67%. This shift may reflect the fact that 31% of companies have already fully implemented cloud solutions and are now shifting their focus to AI.

Non-generative AI has emerged as the second most prioritised technology, with 61% of finance leaders citing it as a focus area—up from 46% earlier this year. Companies are allocating up to 15% of their IT budgets to AI initiatives, signalling growing confidence in its transformative potential.

Overcoming barriers to adoption

Despite these advances, significant challenges remain. Data privacy and cybersecurity top the list of concerns, with 57% of finance leaders identifying them as major barriers to AI adoption. To address these issues, many companies are developing corporate principles for responsible AI use (66%) and involving technology leaders in integration discussions (52%).

Governance is also gaining attention. An increasing number of organisations (39%) plan to include AI risks and associated controls within their financial reporting processes. Private companies, in particular, are leading the charge, with 44% reporting actions to procure third-party controls assurance for AI.

“The demand for controls assurance over AI continues a broader trend of companies perceiving technology-centric risks to pose the biggest potential threats to the integrity of financial reporting,” said Matt Johnson, KPMG US Audit National Technology Assurance Leader.

Planning smarter not harder

The survey underscores a critical turning point for finance leaders. While many are still in the early stages of their AI journey, the benefits for those who advance rapidly are clear. CFOs and CIOs have an opportunity to collaborate more closely, aligning technology investments with business objectives to drive performance and innovation.

“The use of AI and GenAI is becoming ubiquitous across accounting, financial planning, risk management and more,” said Scott Flynn, KPMG US Vice Chair – Audit. “Companies are seeing significant returns on their digital transformation efforts as they integrate these technology capabilities into their financial reporting processes.”