Implementing zero trust security frameworks in banking

Zero Trust security marks a key change in cybersecurity strategy, moving away from assuming trust inside a network. Instead, it’s all about “never trust, always verify,” requiring strict checks for every user, device, and app accessing resources. This is becoming essential for banks facing rising cyber threats, pushing them to adopt stronger security setups.

-

Nikita Alexander

- April 8, 2025

- 5 minutes

Zero Trust security signifies a fundamental shift in cybersecurity strategy. It departs from the traditional perimeter-based approach, which assumes inherent trustworthiness for anything residing inside the network. Instead, the Zero Trust model operates on the principle of “never trust, always verify.” Consequently, every user, device, and application, whether inside or outside the network, must undergo rigorous authentication and authorization before gaining access to resources.

This approach has become increasingly critical for banks and financial institutions. These organizations, after all, represent prime targets for cyberattacks owing to the vast amounts of sensitive data and financial assets they manage. Cybercriminals continually develop sophisticated techniques to bypass traditional security measures. Therefore, banks must adopt more robust security frameworks.

Key principles of zero trust implementation

Implementing Zero Trust in a banking environment necessitates a comprehensive approach centered around several key principles:

-

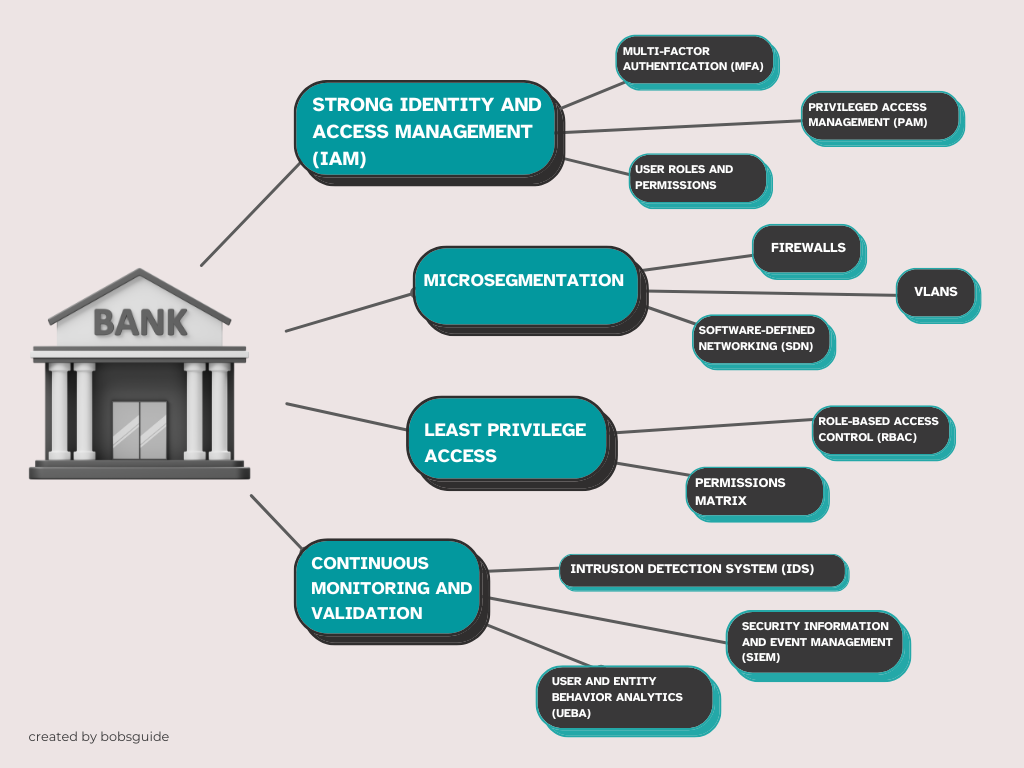

Strong Identity and Access Management (IAM): IAM establishes the foundation of Zero Trust. Banks must deploy robust IAM systems to verify the identity of every user and device seeking access to resources. This includes the use of multi-factor authentication (MFA), which requires users to provide multiple forms of verification, such as passwords, one-time codes, or biometric authentication. Furthermore, privileged access management (PAM) is crucial for controlling and monitoring access to sensitive systems and data by privileged users, such as administrators.

-

Microsegmentation: Microsegmentation involves dividing the network into smaller, isolated segments. This technique effectively limits the lateral movement of attackers within the network. For example, if an attacker gains access to one segment, they cannot easily move to other segments to access critical systems or data. Banks can implement microsegmentation by using firewalls, virtual LANs (VLANs), or software-defined networking (SDN).

-

Least Privilege Access: The principle of least privilege dictates that users should only have the minimum level of access necessary to perform their1 job duties. This, in turn, minimizes the potential damage if an attacker compromises a user’s account. To achieve this, banks should carefully define user roles and permissions to ensure that employees can only access the specific applications and data they require.

-

Continuous Monitoring and Validation: Zero Trust demands continuous monitoring of all network traffic, user behavior, and device activity. To facilitate this, banks should deploy security tools to detect anomalies and suspicious behavior in real-time. These tools include intrusion detection systems (IDS), security information and event management (SIEM) systems, and user and entity behavior analytics (UEBA).2 By continuously validating access and monitoring activity, banks can quickly identify and respond to potential threats.

-

Device Security: Within a Zero Trust environment, every device that accesses the bank’s network must be secured and validated. This encompasses laptops, desktops, mobile devices, and servers. Consequently, banks should implement endpoint security solutions to protect devices from malware and other threats. In addition, they should enforce device compliance policies to ensure that all devices meet specific security requirements, such as having up-to-date software and antivirus protection.

In practice

Implementing Zero Trust in a bank is, without a doubt, a complex process that demands careful planning and execution. Here’s a suggested approach:

-

Assess the Current Security Posture: Initially, banks should assess their existing security infrastructure and identify any gaps or vulnerabilities. This assessment should include a review of network architecture, identity and access management systems, and security policies.

-

Define Clear Goals and Objectives: Subsequently, banks should define specific and measurable goals for their Zero Trust implementation. These goals might include reducing the risk of data breaches, improving compliance with regulations, or enabling secure remote access.

-

Prioritize Critical Assets: Following goal definition, banks should identify their most critical assets, such as customer data, financial records, and core banking systems. Furthermore, they should prioritize the protection of these assets in their Zero Trust implementation.

-

Implement IAM and MFA: Deploying robust IAM systems and MFA represents a crucial first step in Zero Trust implementation. This will help banks gain better visibility and control over user access.

-

Implement Microsegmentation: Next, banks should segment their networks based on the sensitivity of the data and applications. This will help to contain the impact of any potential breach.

-

Enforce Least Privilege: In addition, banks should review and refine user permissions to ensure that users only have the necessary access. This may involve implementing role-based access control (RBAC).

-

Deploy Continuous Monitoring Tools: Moreover, banks should implement security monitoring tools to detect and respond to threats in real-time. These tools should provide visibility into network traffic, user behavior, and device activity.

-

Automate Security Responses: To improve efficiency and reduce response time, banks should automate security responses to common threats. This may involve using security orchestration, automation, and response (SOAR) tools.

-

Regularly Review and Update: Finally, it is important to remember that Zero Trust is not a one-time implementation but an ongoing process. Banks should regularly review and update their Zero Trust framework to adapt to evolving threats and business needs.

Challenges and considerations

While Zero Trust offers significant security benefits, banks may encounter several challenges during implementation:

-

Complexity: Undeniably, implementing Zero Trust can be complex and may require significant changes to existing infrastructure and processes.

-

Cost: Furthermore, implementing Zero Trust can be expensive, requiring investments in new technologies, training, and expertise.

-

Legacy Systems: Additionally, many banks rely on legacy systems that may not be compatible with Zero Trust principles. Integrating these systems into a Zero Trust framework can be challenging.3

-

User Experience: Finally, balancing security with user convenience is crucial. Overly restrictive security measures can hinder productivity and user adoption.

Zero Trust security constitutes a critical strategy for banks seeking to protect themselves from increasingly sophisticated cyber threats. By implementing Zero Trust principles, banks can enhance their security posture, reduce the risk of data breaches, and improve compliance with regulatory requirements.4 Although implementation presents challenges, the long-term benefits of Zero Trust make it a necessary investment for the financial sector.