How bank-based payout services are holding your business back

Emerging technologies have changed practically every facet of our daily lives. From smartphones to flying drones, the pace of innovation continues to accelerate at almost maddening speeds. But, as is the case with any race, there are those who get left behind. While still functional, legacy technology can often create more problems than solutions; sure,

-

Luke Trayfoot

- June 3, 2019

- 6 minutes

Emerging technologies have changed practically every facet of our daily lives. From smartphones to flying drones, the pace of innovation continues to accelerate at almost maddening speeds. But, as is the case with any race, there are those who get left behind. While still functional, legacy technology can often create more problems than solutions; sure, technically you can make a call on a rotary phone, but what happens when you need to press “1” to talk to the operator? The same can be said for legacy payment services offered through traditional financial institutions.

If tech’s motto is, “move fast and break things,” the financial sectors would be, “crawl forward and tread lightly,” and for good reason. These institutions are responsible for supplying the world with credit, safeguarding the deposits of the masses, and ultimately keeping the economy above water. It’s an important task, and one that requires a great deal of skepticism, especially when it comes to change. But change is the lifeblood of innovation in today’s fast-paced digital age. At a time when online marketplaces are implementing processes to continuously improve their customer checkout experience, many of the EU’s top digital merchants are still settling for archaic bank transfer technology when it comes to processing their seller or freelancer payouts. Little do they know, settling for the status quo isn’t just slowing down their payout process, it’s also limiting the recruiting power on their marketplace, opening their organization to regulatory and data security concerns, and hampering supply-side satisfaction. Solving these sorts of issues, both now and as your marketplace evolves, will require out-of-the-box (or rather, out-of-the-bank) thinking. It’s time to consider a payout platform approach.

You don’t know what you’re missing

When it comes to payout innovation, it’s time to come to terms with the fact that bank transfers simply won’t cut it. To explain this, let’s look at three major areas of difference between a typical bank transfer payout process and a fintech-fueled platform approach.

Efficiency

· Banks are creatures of process. Unfortunately, these regimented processes don’t lend themselves to iteration or individuation all that easily. One-size fits all, take ‘er or leave ‘er. While this black and white approach to operations makes things easy for the bank, it ultimately forces businesses to solve for a wide range of inefficiencies.

· Payout platforms are designed to not just solve these inefficiencies, but also can help provide value-added services that will further streamline merchant operations and payee process.

|

|

Bank transfers |

Payout platform |

|

Efficiency |

|

|

|

|

|

|

|

User experience

· As mentioned before, banks cater to broad audiences and thus are driven to provide a relatively generic user experience. Business banking services are designed to accommodate any and every business, regardless of unique industry needs. Their focus is managing risk, whereas more agile fintech players can build highly specialized services designed to meet the unique needs of specific industries and evolving business models.

· Payout platforms focus their efforts on streamlining functionality. From accessibility to speed, personalization to convenience, the technology deployed by payout platforms is focused on enriching both the merchant and the payee’s overall experience.

|

|

Bank transfers |

Payout platform |

|

User experience |

|

|

|

|

|

|

|

Expansion efforts

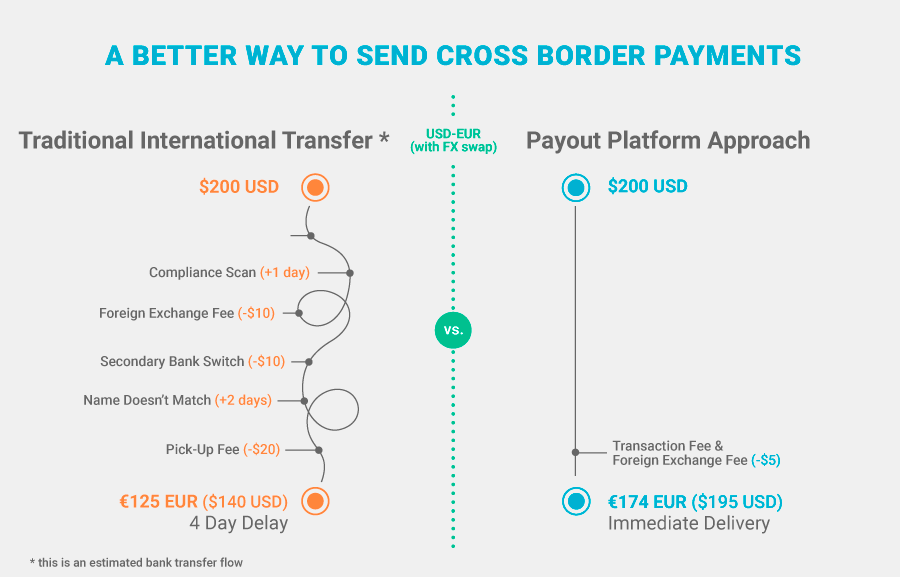

· Sending money between bank accounts in different countries is a painful and expensive experience. That’s because there is no such thing as an international clearing system. In order for a merchant to send money globally, that single payment will need to ride multiple international financial rails in order to get to its final location. It’s often a very manual way to send money cross-border, and one that becomes frustratingly inefficient and unbelievably expensive when you need to send a high volume of lower value payments on a weekly or even daily basis, as is the case for most marketplace platforms.

· As correspondent banking becomes increasingly tedious, payment providers have jumped on the opportunity to build a better, faster, and smarter way to send money globally. While banks are already connected to their country’s local clearing networks (think SEPA), payout platforms are working to connect these global real-time clearing networks to each other.

|

|

Bank transfers |

Payout platform |

|

Expansion efforts |

|

|

|

|

|

|

|

|

|

These days, you wouldn’t fax a client now that email provides a better, faster mode of communications, so why send your contractor an untraceable bank transfer when you could just as easily provide them the option of collecting their payments with PayPal or real-time to a prepaid card? Leave legacy bank-based payout processes in the past where they belong. Now’s the time to Invest in a payout platform that improves operational efficiencies, enhances the overall user experience for a wide range of payees, and is primed for expansion.