Global payments 2024: The hidden complexity of simpler payments

Global payments may feel simpler, but behind the scenes, complexity is rising. McKinsey’s 2024 report shows that while users enjoy faster interfaces, providers face growing challenges from fragmented systems, regulations, and fintech competition. For executives, navigating these trends is key to staying competitive.

-

Marina Mouka

- October 21, 2024

- 5 minutes

As global payments evolve, users are increasingly experiencing seamless and efficient interfaces. Yet behind these advances lies a growing complexity that continues to reshape the landscape. The 2024 report by McKinsey & Company highlights this paradox, revealing that while the customer experience may be smoother, the infrastructure that supports it is becoming increasingly multifaceted.

Over the past decade, payment providers have embraced new technologies, expanding the range of services and enabling faster, more convenient transactions. However, these advances come at the cost of growing fragmentation within the payment value chain, more intermediaries, and heightened regulatory demands. For C-suite executives navigating this environment, the future of global payments presents both opportunities and challenges.

Continued revenue growth, but at a slower pace

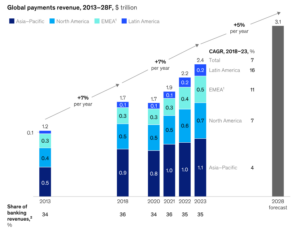

Between 2018 and 2023, the global payments industry grew steadily, with revenues reaching $2.4 trillion. However, this growth is projected to slow from 7% to 5% annually over the next five years. By 2028, global payments revenue is expected to hit $3.1 trillion—an increase of $700 billion. This underscores the need for banks and financial institutions to continue investing in cutting-edge payment technologies if they hope to maintain a competitive edge over specialist providers, whose market share has surged in recent years.

Source: McKinsey Global Payments Map

Over the past decade, the market capitalisation of specialist payment firms has ballooned from $400 billion to $1.4 trillion, a clear indication that nimble, technology-driven players are dominating the space once led by traditional financial institutions. Yet, while these firms are capitalising on new opportunities, incumbents are by no means standing still.

Six key trends shaping the future

According to McKinsey’s analysis, six trends will dominate the payments landscape over the next five years:

-

The decline of cash

The global shift away from cash continues, though at different paces across regions. In developed markets like the United States and Germany, cash usage remains low, with only 5% of consumer payments in the US still made with physical currency. Meanwhile, in emerging economies like India and Indonesia, instant payments are rapidly replacing cash, with India projected to reduce cash transactions from 23% to below 10% by 2028.

-

Instant payments on the rise

Instant payment systems are now operational in most major markets and are set to grow exponentially, particularly in regions like the European Union. The volume of instant payment transactions in Europe is expected to increase tenfold by 2028. However, the adoption of instant payments faces different hurdles in card-dominated markets like the UK, where credit and debit cards remain deeply entrenched.

-

Digital public infrastructure (DPI)

Nations like Brazil and India are leading the charge in developing DPI, which has enabled more inclusive and efficient payment ecosystems. Emerging economies such as Indonesia and Nigeria are expected to follow suit, implementing DPI solutions to facilitate broader financial inclusion.

-

Rise of platforms and marketplaces

The shift to e-commerce platforms like Amazon and Shopify is altering the way payments are processed. These platforms now account for 30% of global consumer purchases, with higher penetration in the SME segment. Financial incumbents are responding with their own solutions, but competition from fintech disruptors like Stripe and Adyen remains fierce.

-

Transaction banking evolution

As corporations demand more seamless and intuitive financial services, transaction banking is moving closer to the user-friendly experience consumers are accustomed to. Institutions like Goldman Sachs and Santander are building standalone transaction banking businesses, capitalising on the demand for more sophisticated and integrated solutions for corporate clients.

-

Central bank digital currencies (CBDCs)

Although early excitement around CBDCs has waned, they remain a key area of development. Over 90% of central banks are exploring digital currencies, and more than 30 have launched pilot programmes. CBDCs are expected to provide a baseline for digital currency functionality, offering an alternative to private stablecoins and helping to regulate the pricing of commercial digital payment offerings.

Investment priorities for future growth

For payment providers seeking to capitalise on the $1 trillion in projected growth, three areas stand out for investment: instant payment solutions, anti-money laundering (AML) and fraud prevention systems, and next-generation payment infrastructures capable of handling real-time transactions at high volumes.

Source: McKinsey

Cross-border payments are a particularly attractive segment, with fintech disruptors like Wise and Airwallex leading the way in retail and SME markets. Treasury management and payroll solutions also present significant opportunities for innovation, with instant payments increasingly becoming a differentiator for corporate services. Employers in the gig economy, for example, are leveraging instant payments to enhance worker satisfaction by providing immediate compensation, a trend that is likely to grow.

Meanwhile, the fight against financial crime is intensifying. Global payment fraud losses are expected to reach $400 billion over the next decade, with regulatory pressures pushing providers to enhance their AML and fraud detection systems. Technologies like AI, combined with real-time data, are emerging as powerful tools in this ongoing battle.

A complex but promising future

As the global payments industry continues to evolve, the road ahead promises both challenges and opportunities. For C-suite executives, the ability to navigate these complexities while staying ahead of regulatory demands and technological disruptions will be key to capturing market share in an increasingly competitive environment.

The ultimate goal of global payments—to be simple, safe, quick, and ubiquitous—is within sight, but achieving it requires strategic investment and a keen understanding of the emerging trends shaping the landscape.