FCA and CMA release UK bank scores in line with Open Banking

The UK's Financial Conduct Authority (FCA) and Competition & Markets Authority (CMA) has released data on quality of service for the first time, marking a historic step for Open Banking and putting a mass of customer data in the hands of fintechs and comparison websites. From today, banks must publish information on how likely both

-

David Beach

- August 15, 2018

- 3 minutes

The UK's Financial Conduct Authority (FCA) and Competition & Markets Authority (CMA) has released data on quality of service for the first time, marking a historic step for Open Banking and putting a mass of customer data in the hands of fintechs and comparison websites.

From today, banks must publish information on how likely both retail and business customers would recommend them, including online and mobile banking offerings, branch and overdraft services to friends, relatives and other businesses. A total of 16,012 customers of UK banks have been surveyed so far.

“For the first time, people will now be able to easily compare banks on the quality of the service they provide, and so judge if they’re getting the most for their money or could do better elsewhere," said Adam Land, Senior Director at the CMA.

All British banks and building societies with more than 150,000 personal current accounts (PCA) or 20,000 business current accounts (BCA), as well as Northern Irish banks and building societies with more than 20,000 PCAs or 15,000 BCAs, must publish the information every six months.

“This is one of the many measures – including Open Banking and overdraft text alerts – that we put in place to make banks work harder for their customers and help people shop around to find the best deals for them,” said Land.

The results of the survey must be prominently displayed in bank branches, as well as on their websites and apps, allowing customers to make better-informed choices around financial services offered to them.

“Getting a good deal isn’t just about pricing," said Christopher Woolard, executive director of strategy and competition at the FCA. "It’s also important for customers – including individuals and small businesses – to be able to judge the quality of service around their current account and to see whether other providers could offer something that suits them better. This information should encourage providers to offer the services that people value.”

Retail banking

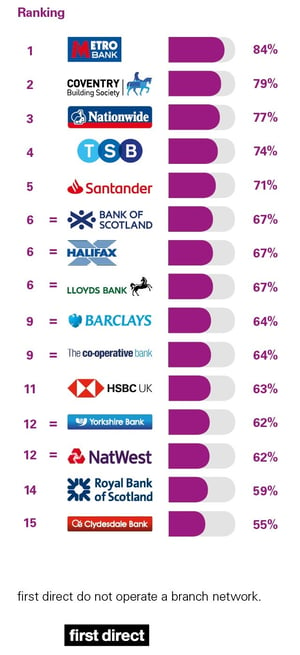

Customers with personal current accounts were asked how likely they would be to recommend their provider, their online and mobile banking services, services in branches and overdraft services to friends and family. The results show the proportion of customers of each provider who said they were ’extremely likely’ or ‘very likely’ to recommend each service. (Source: GFK)

Overall service quality

Online and mobile banking services

Overdraft services

Services in branches

Business banking

SME business customers were asked how likely they would be to recommend their provider, their online and mobile banking services, services in branches and business centres as well as SME overdraft and loan services and relationship/account management services, to other SMEs. The results show the proportion of customers of each provider who said they were ‘extremely likely’ or ‘very likely’ to recommend each service. (Source: BDRC)

Next steps

Further to this, the FCA has informed banks that, from November 2018, they will have to publish information highlighting the support they offer customers along the following criteria:

- Resilience – low ability to withstand financial or emotional shocks

- Life events – major life events such as bereavement or relationship breakdown

- Capability – low knowledge of financial matters or low confidence in managing money

- Health – conditions or illnesses that affect ability to carry out day to day tasks

From February 2019, providers will also be required to publish quarterly information on how long it takes to open a current account and to replace a debit card.